Economists expected a 0.1 percentage point rise in the PPI. The BLS reports 0.2 with May revised up by 0.2 percentage points. Services inflation is hot except trucking.

Last month I reported The Producer Price Index Unexpectedly Declines in May

Strike that headline thought. This month the BLS Revised the PPI Higher.

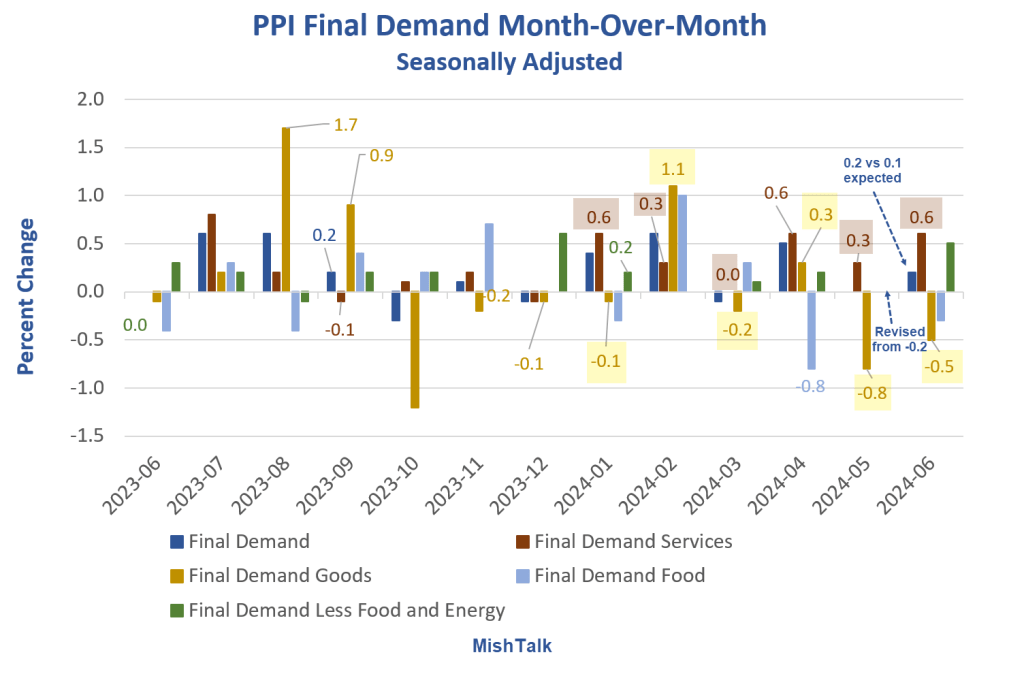

PPI Final Demand Month Over Month

- Overall: 0.0 Percent

- Goods: -0.5 Percent

- Services: 0.6 Percent

- Food: -0.3 Percent

- Excluding Food and Energy: 0.4 Percent

Goods vs Services

- Goods: For the first six months of 2024, starting January, PPI Goods were -0.1, 1.1, -0.2, 0.3, -0.8, -0.5. That’s a slightly negative monthly average.

- Services: For the first six months of 2024, starting January, PPI Services were 0.6, 0.3, 0.0, 0.6, 0.3, and 0.6. That’s an average monthly of 0.4.

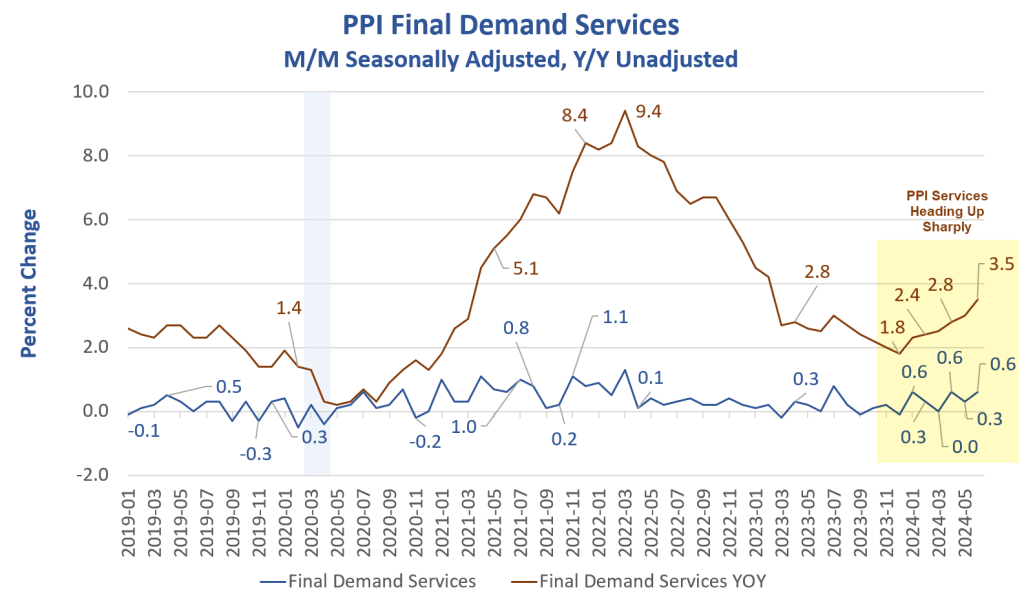

Final Demand Services

Prices for final demand services rose 0.6 percent in June after moving up 0.3 percent in May. Nearly all the June increase is attributable to a 1.9-percent jump in margins for final demand trade services. (Trade indexes measure changes in margins received by wholesalers and retailers.)

The index for final demand services less trade, transportation, and warehousing inched up 0.1 percent. Prices for final demand transportation and warehousing services fell 0.4 percent.

Over one-quarter of the June advance in prices for final demand services can be traced to a 3.7-percent rise in margins for machinery and vehicle wholesaling.

Prices for truck transportation of freight declined 1.2 percent. The indexes for residential real estate loans (partial) and for machinery and equipment parts and supplies wholesaling also decreased.

Final Demand Goods

Prices for final demand goods moved down 0.5 percent in June after falling 0.8 percent in May. Most of the June decrease is attributable to a 2.6-percent drop in the index for final demand energy. Prices for final demand foods declined 0.3 percent, while the index for final demand goods less foods and energy was unchanged.

Over 60 percent of the June decrease in the index for final demand goods can be traced to a 5.8-percent decline in prices for gasoline. The indexes for processed poultry, residential electric power, diesel fuel, jet fuel, and fresh and dry vegetables also moved lower. Conversely, prices for chicken eggs increased 55.4 percent. The indexes for residential natural gas and for aluminum base scrap also advanced.

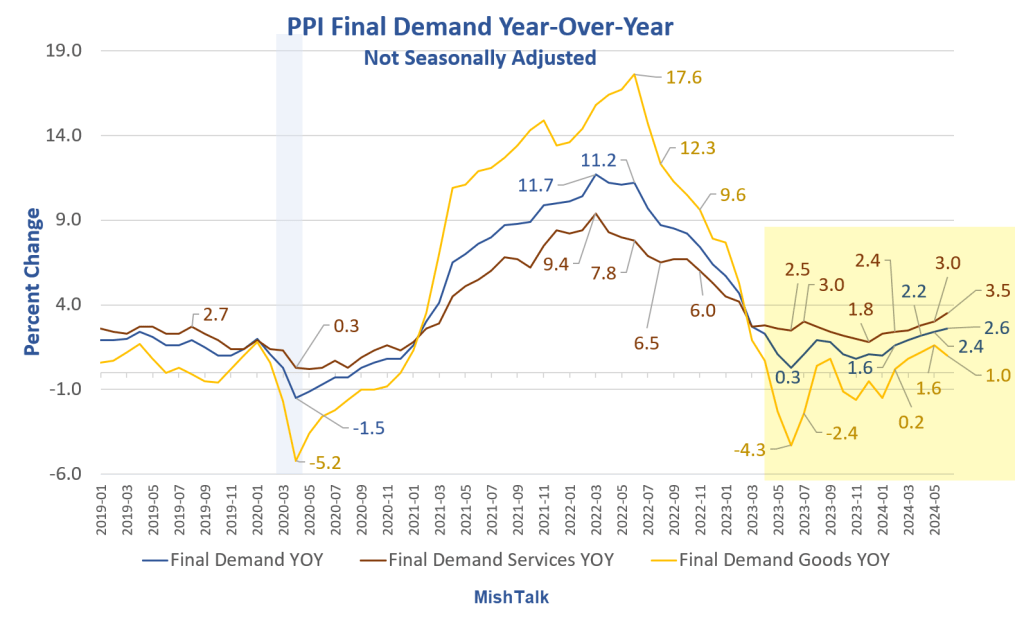

PPI Final Demand Year-Over-Year

The year-over-year PPI for both goods and services has bottomed. Services are a disaster.

PPI Final Demand Services Y/Y and M/M

Year-Over Year Details

- Final Demand: +2.6 Percent

- Final Demand Goods: +1.0 Percent

- Final Demand Services: +3.5 Percent

- Final Demand Less Food and Energy: 3.0 Percent

- Final Demand Energy: -1.4 Percent

Services impacts the PPI more than goods. It’s the services number the Fed will pay attention to the most.

Very Bad Report

This report is very bad, if not terrible, for the Fed. The cost of services is rising which adds to overall inflation pressures.

Falling energy and trucking services strongly suggests (along with many other things) a slowing economy.

CPI Declines in June, Rent Finally Moderates, Food Away From Home Is a Problem

Yesterday, I reported CPI Declines in June, Rent Finally Moderates, Food Away From Home Is a Problem

The string of 33 consecutive months of rent rising 0.4 percent or more is finally broken.

That’s the good news. The bad news is the price of food away from home rose another 0.4 percent.

The seemingly good news is the price of gasoline fell 3.8 percent. But why is the price of gasoline falling? Here’s the answer:

Recession Has Begun

On July 8, I stated Weak Data Says a Recession Has Already Started, Let’s Now Discuss When

Weakness Everywhere

There is weakness in housing (new home sales, existing home sales, and starts at the lowest in 4 years), consumer spending, manufacturing (both durable and nondurable good), jobs data (constant negative revisions, QCEW, major survey discrepancies, quits, and a rising unemployment rate), and finally we have major unexpected ISM Services in Contraction.

All of the above items are hard data other than the services ISM.

There is no savior on the horizon this time. The Fed rates to be inactive until it panics in September and that will be much too late to stop a recession that started in May or June.

The recession will cool energy and rent is cooling on its own.

For more details and discussion as to why I think a recession has started, please see the above link.